25 Practical Tipid Tips That Help You Save Money Faster in the Philippines

Disclaimer: This post is not a financial or investing advice, it’s for educational purposes only. It may contain affiliate links, meaning I get a commission if you decide to make a purchase, at no extra cost to you. Read our disclosure

Our heavenly rice is getting expensive every day. Meralco bills sting. Even a quick trip to the palengke can destroy your budget faster than expected.

So yes, saving money in the Philippines can feel like a hassle.

And when petsa de peligro hits, it gets worse. You check your wallet, open your banking app, and then ask yourself the same question: “saan napunta ang sahod ko?”

If that sounds familiar, then keep reading.

Here’s the thing: building your savings does not require a 6-figure income. It usually starts with smaller moves. The boring and repeatable ones. The daily choices that don’t look dramatic at first, but quietly give you breathing room month after month.

This guide is for Filipino professionals who want practical, no-drama advice. No vague lectures. No “just earn more” nonsense. Just 25 realistic tipid tips you can actually use, whether you’re trying to budget your salary, survive rising prices, or finally hit your ipon goals.

Change your Money Mindset first

Before the grocery hacks, before the Meralco tricks, before the “cancel your subscriptions” speech, you need to fix how you think about money.

Because your habits follow your mindset. Every time.

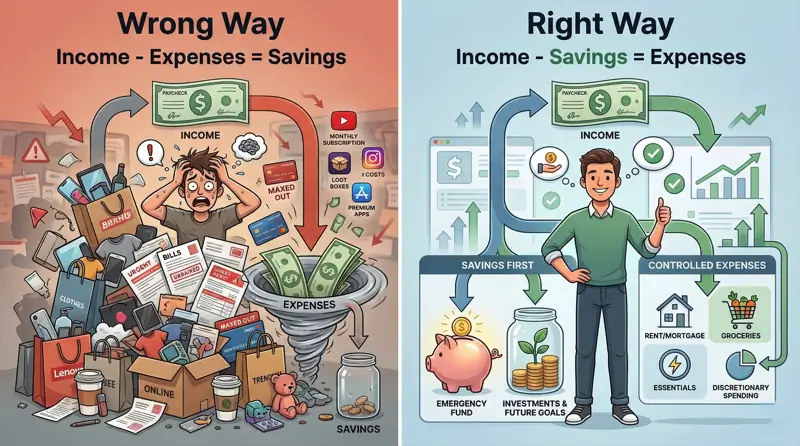

Pay yourself first

Most people do this:

That’s the problem. By the time bills, food, transpo, and random gastos hit, there’s usually nothing left.

Try this instead:

The moment your salary lands in your payroll account, move 10% to 20% straight into a separate savings account.

Don’t wait. Don’t overthink it. Treat savings like rent: something you need to pay, not something you “hope” to have left over.

Use the 50-30-20 rule, then adjust it to real life

50-30-20 budgeting rule works because it’s simple.

Split your net income into three buckets:

- 50% for needs – rent, groceries, bills, pamasahe

- 30% for wants – eating out, subscriptions, shopping, gala

- 20% for savings or debt payments – emergency fund, loans, investments

That said, real life in the Philippines isn’t always neat. If your rent is high or you support family, you may need to tweak the percentages. That’s okay. The point is to give every peso a job.

Put impulse buys on a 24-hour hold

Shopee. Lazada. TikTok Shop. One tap, one budol.

That’s why you need a rule.

If you see something tempting, add it to cart. Then leave it there for 24 hours. No checkout. No excuses.

Most of the time, the urge fades. You realize you didn’t need that desk organizer, “sale” hoodie, or kitchen gadget in the first place. And if you still want it after a day, at least you’re buying with a clear head, not with midnight dopamine.

Watch out for lifestyle creep

You get a raise. Nice. Then suddenly your spending levels up too.

You start taking Grab more often. You upgrade your phone earlier than planned. Your occasional café coffee becomes a daily ₱180 habit. It feels harmless at first. It adds up fast.

That’s lifestyle creep.

When your income grows, your expenses don’t need to copy-paste the same behavior. Keep your old budget for as long as you can, then send the extra money to savings, investments, or debt payments. That’s how raises actually improve your life.

Track every peso

You can’t fix what you don’t measure.

A lot of people say their salary just “disappears.” But money rarely disappears. It leaks. Small food deliveries. Random convenience store runs. Online checkouts you forgot about. Extra rides because tinamad maglakad.

Track every expense for at least one month.

Use whatever works:

- a notebook

- Google Sheets

- a budgeting app

- even your Notes app

The method matters less than the habit. Once you see where your cash really goes, cutting back gets easier.

Food and Grocery Hacks: “Busog pero hindi wasak ang budget”

For many Filipino households, food eats up the biggest part of the monthly budget. Understandable. Between grocery runs, family meals, takeout, and delivery apps, this category can get out of hand quickly.

The good news? Food is also one of the easiest places to save.

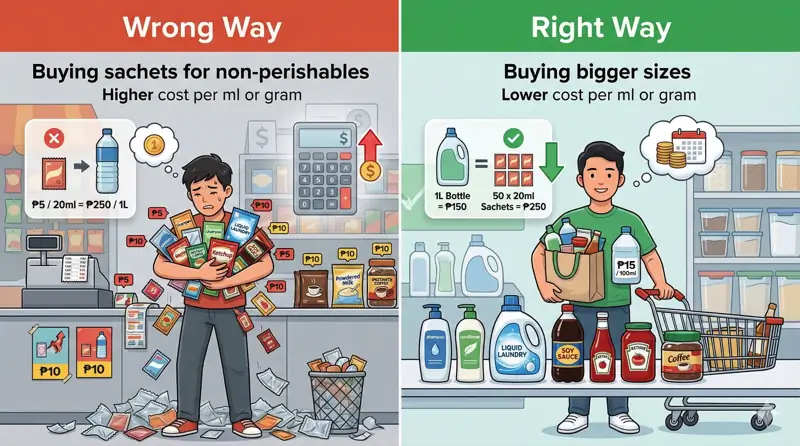

Stop relying on tingi when you can buy bigger packs

Buying sachets feels cheaper because the cash out is smaller. That’s why “tingi” culture is so common, especially when money is tight.

But compute it by gram or milliliter and you’ll see the catch: tingi usually costs more.

That ₱7 shampoo sachet or small pack of coffee looks budget-friendly today, but repeated over a month, you often spend more than you would on a larger bottle or pack.

So when cash flow allows, buy non-perishable basics in bigger sizes:

- shampoo

- detergent

- coffee

- cooking oil

- condiments

You’ll spend more upfront, yes. But less overall.

Plan a weekly tipid ulam menu

Going to the grocery without a plan is dangerous. You tell yourself you’ll “just buy a few things,” then somehow leave with snacks, frozen treats, and ingredients for meals you won’t even cook.

A weekly meal plan fixes that.

Build your menu around affordable staples and seasonal ingredients. Think:

- eggs

- tokwa

- munggo

- sardines

- chicken

- local vegetables in season

This doesn’t need to be fancy. Kahit simple lang. What matters is you know what you’re cooking for the week, so you only buy what you need and waste less food.

Never grocery shop while hungry

This sounds basic. It works.

When you shop on an empty stomach, everything feels urgent. Chips become a “reward.” Fancy biscuits become “pang-merienda.” Suddenly your cart is full of cravings, not essentials.

Eat first. Then bring a list. Then follow the list.

That one habit alone can save you more than you think.

Cook at home more often than you order in

GrabFood and food delivery apps are convenient. After a long workday, they feel like salvation.

But they’re expensive. Fast.

A meal listed at ₱150 can end up costing almost double once you add delivery fees, service fees, and tips. Do that a few times a week and your budget starts bleeding.

Cooking at home wins almost every time. Even better, batch-cook on your day off so you’re not forced to decide when you’re already tired.

Meal prep is not glamorous. But it works.

Buy fresh ingredients at the palengke

Air-conditioned supermarkets are comfortable. The palengke is not always comfortable. Let’s be honest.

It can be hot, crowded, and a bit chaotic.

But prices are often better there, especially for:

- vegetables

- fish

- meat

- fruits

Go early if you can. Compare stalls. Ask for tawad or dagdag. That’s one thing you can’t do in a grocery chain.

For many families, the local wet market is still one of the best places to stretch a food budget.

Bring baon to work

This is one of the strongest tipid hacks out there. Simple. Effective. A little annoying at first.

If you buy lunch for ₱150 every workday and grab a ₱150 coffee on top of that, you could easily spend ₱6,000 or more a month just on workday food and drinks.

That’s a painful number.

Bring your own baon. Bring your own tumbler. Brew coffee at home if you can. Even doing this three to four times a week can free up serious cash for your emergency fund.

How to Cut Utility Bills Without Making Life Miserable

Utility bills in the Philippines hit hard, especially during summer. Open the statement, stare for three seconds, then pretend maybe there’s a billing mistake.

Sometimes there isn’t.

Still, you’re not helpless here. A few changes at home can lower your monthly bills without turning your house into a dark, sweaty cave.

Switch to inverter appliances and LED bulbs

Old appliances are budget killers.

If your aircon or ref is non-inverter and already struggling, it may be draining more electricity than you realize. The same goes for outdated bulbs.

LED lights and inverter appliances usually cost more at the start. That part hurts. But they often use much less electricity, which can make the upgrade worth it over time, especially for appliances you use every day.

Unplug devices you’re not using

Some electronics still draw power even when they look “off.” Chargers, TVs, microwaves, desktop setups, these little drains add up.

Make it a habit to unplug what you don’t need.

Or better, use a power strip with one switch so you can shut down several devices at once. Easy win.

Use your aircon and fan together

You do not need to blast the aircon all night at full power just to sleep well.

Try this: cool the room first, set a timer for two to three hours, then let an electric fan keep the air circulating after the aircon turns off.

It’s a practical middle ground. Less gastos, less guilt, still decent sleep.

Fix leaks right away

A dripping faucet looks harmless until you remember you’re paying for that water.

Same with a toilet that keeps running.

Leaks waste money every single day, and the frustrating part is they’re easy to ignore because the damage feels small in the moment. But over weeks or months, that “small” waste becomes a bigger bill.

If you spot a leak, deal with it now. Not “next week.”

Defrost older refrigerators regularly

If you still use an older ref that isn’t frost-free, check the freezer. Ice buildup makes the appliance work harder, which can push your electricity use higher.

Regular defrosting helps it run more efficiently.

Not exciting. Not Instagram-worthy. But definitely tipid.

Transportation and Commuting Hacks

Transportation costs sneak up on people. A few rides here. A Grab there. Toll fees. Parking. Gas. Then you total everything at month-end and wonder why your wallet looks defeated.

Here are a few ways to trim that expense.

Walk or bike short distances

If your destination is close, say one or two kilometers, skip the tricycle or short ride when it’s safe and realistic to do so.

Walking saves money. Biking saves money. Both also help you move more, which is a nice bonus.

Those ₱20 to ₱50 rides don’t feel serious in the moment. Repeat them daily, though, and they become real money.

Use public transport or carpool more often

Owning a car in the Philippines is expensive beyond the monthly gas budget. There’s fuel, parking, tolls, maintenance, and the random repair bill that shows up at the worst possible time.

If you can leave the car at home a few days a week, do it.

The MRT, LRT, buses, jeepneys, UV Express, and carpools can still save you a lot, even if commuting comes with its own headaches. It’s not always comfortable. It’s not always convenient. But for many people, it’s cheaper by a mile.

Plan your route before you leave

Traffic burns fuel. It also burns patience.

Before driving, check Waze or Google Maps. Look for road closures, bottlenecks, and faster alternate routes. If your schedule is flexible, avoid peak hours when possible.

A smarter route won’t magically erase Metro Manila traffic. Nothing can. But it can cut wasted fuel and time.

Maintain your vehicle properly

If you rely on a car or motorbike, regular maintenance is not optional. It’s part of saving money.

Underinflated tires can hurt fuel efficiency. Dirty filters, overdue oil changes, and neglected engine issues can make things worse. Then one small problem becomes an expensive repair.

Check tire pressure. Follow your maintenance schedule. Don’t wait until something sounds alarming.

That “I’ll deal with it later” mindset usually costs more.

Lifestyle, Subscriptions, and Banking Moves That Actually Help

This last section is where a lot of quiet money leaks happen. Not through giant purchases but through recurring charges, convenience spending, and habits that seem harmless because they’re small.

Let’s clean that up.

Audit your subscriptions

Open your bank app, GCash, Maya, or credit card statement. Then look for recurring payments.

Be honest with yourself.

Are you really using all those streaming apps? Are you still going to that gym? Is that premium membership still worth it, or did you forget to cancel it three months ago?

Subscriptions are sneaky because they feel low-maintenance. They’re also easy to ignore.

If you haven’t used it in the last 30 days, cut it. You can always subscribe again later.

Use online sales wisely, not emotionally

Double-digit sales like 3.3, 6.6, 9.9, 11.11, and 12.12 can help you save but only if you already planned the purchase.

That’s the key.

Use these sale dates for:

- non-perishable household items

- personal care products

- school or office supplies

- higher-ticket items you already researched

Stack vouchers. Compare sellers. Watch out for fake discounts. And never call it “tipid” if the item wasn’t needed in the first place.

A discounted unnecessary purchase is still unnecessary.

Buy pre-loved items

Secondhand shopping isn’t something to be embarrassed about. For many Filipinos, it’s just smart.

Check:

- ukay-ukay

- Facebook Marketplace

- Carousell

- community buy-and-sell groups

You can find quality clothes, furniture, home items, and sometimes even gadgets at a much lower price than retail. Just inspect carefully before paying, especially for electronics and appliances.

Put your savings in the right bank account

Saving is step one. Making your money work harder is step two.

Many traditional savings accounts offer low interest, so your money barely grows. That’s why many Filipinos now look at BSP-regulated digital banks for better rates, especially for emergency funds and short-term savings.

Before opening an account, check:

- whether the bank is regulated by the BSP

- the current interest rate

- deposit limits or requirements

- transfer fees

- app reliability

- PDIC coverage details

The goal is simple: don’t let your money sleep in the wrong place.

Learn to say no

This one is hard. Sometimes harder than budgeting.

You’ll get invited to dinners, inuman sessions, out-of-town trips, weddings, group gifts, last-minute gimmicks, and all sorts of gastos that don’t fit your budget. And because you don’t want to look kuripot, you say yes.

Then you regret it later.

You are allowed to say no.

You are allowed to suggest a cheaper plan.

You are allowed to skip something that messes up your personal finances.

Real friends won’t shame you for having boundaries. And if they do, that’s a different problem.

Final Thoughts

Saving money fast in the Philippines is not about depriving yourself of every little joy. It’s about being more intentional with your cash so you stop feeling one emergency away from panic.

That’s the real win.

You don’t need to apply all 25 tips overnight. Start with three. Build momentum. Then add more as your habits improve. Small actions count, especially the ones you repeat.

Before you know it, petsa de peligro won’t feel as brutal. Your bills will feel more manageable. Your savings will start to look real. And that kind of progress? Ang sarap nun.

What’s your go-to tipid hack?

Share it in the comments and swap ideas with the Juan Investor community.