If You’re Always Broke After Payday, Try the 50/30/20 Budget Rule

Disclaimer: This post is not a financial or investing advice, it’s for educational purposes only. It may contain affiliate links, meaning I get a commission if you decide to make a purchase, at no extra cost to you. Read our disclosure

You get your sweldo on the 15th, pay a few bills, treat yourself to a nice meal, and suddenly it is the 20th. Your wallet is now empty.

Welcome back to petsa de peligro.

Making money is hard enough. But figuring out where every single peso goes? That is exhausting. Tracking every jeepney fare, every iced coffee, and every random Shopee checkout usually leads to budget burnout.

You try a complex spreadsheet for a week, get frustrated, and give up entirely by week 2.

You don’t need a complicated accounting system to survive the Philippine economy. You need a simple boundary.

That’s where the 50/30/20 rule comes in.

It’s a simple budgeting framework that answers one big question:

How do I budget my salary in the Philippines without overcomplicating it?

Today, we are going to strip away the Americanized advice and tailor this exact formula to the harsh realities of living, working, and spending in the Philippines.

This guide will show you:

- What the 50/30/20 rule really means

- How to apply it in the Philippine setting

- Sample salary breakdown

- Adjustments if your income is tight

- Practical budgeting tips Pinoy professionals actually use

Let’s break it down.

By the end, you’ll have a simple, actionable system to budget your salary without feeling restricted or overwhelmed.

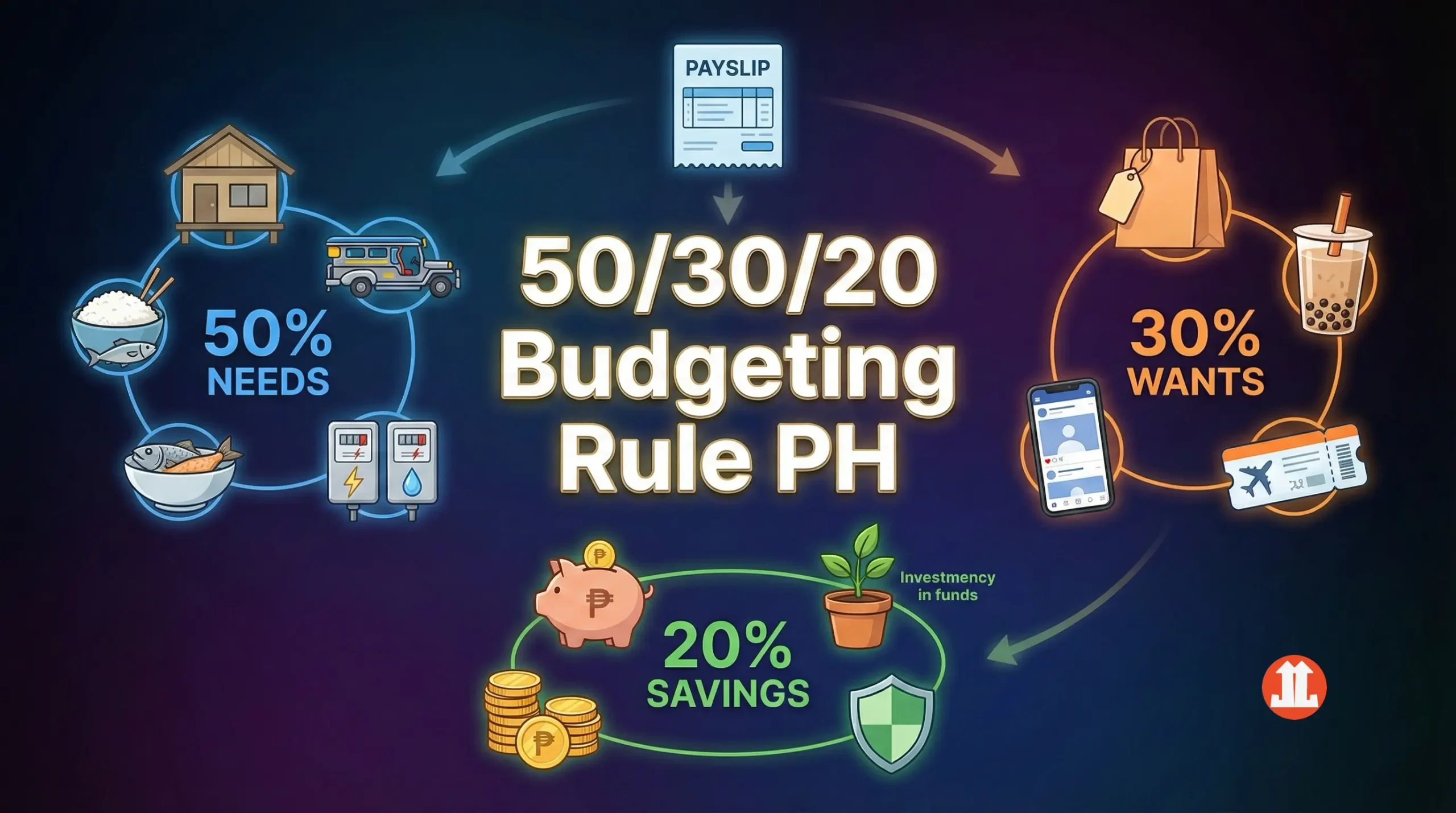

What is the 50/30/20 Rule?

The 50/30/20 rule is a percentage-based budgeting strategy. Instead of agonizing over fifty different micro-categories, you divide your net income into just three buckets.

Keep in mind, we are talking about your net income: the actual cash that hits your payroll account after the BIR, SSS, PhilHealth, and Pag-IBIG have taken their mandatory cuts.

Here is the exact breakdown:

50% for Needs (Non-Negotiables)

These are expenses you absolutely cannot survive without. If you lose your job tomorrow, these bills still arrive. This bucket covers your rent, Meralco and Maynilad bills, and basic palengke or grocery runs.

30% for Wants (Guilt-free Spending)

This is the secret sauce to making a budget stick. Budgeting feels like a prison when you cut out all joy. You allocate this 30% for GrabFood deliveries, Netflix subscriptions, weekend cafe runs, or setting aside extra cash to buy gifts for your nephews. You work hard. You deserve to enjoy the fruits of your labor.

20% for Savings and Debt (Financial Future)

This is where wealth is built. This bucket pays for your peace of mind. You use this 20% to build your emergency fund, aggressively pay off toxic credit card balances, and eventually fund your investments.

It is that simple. No complex math. Just three clear boundaries that tell your money exactly where to go.

Breaking down your “Needs” (50%)

The Non-Negotiables

What exactly is a “need“? It’s an expense you cannot survive without. If you lose your client or get laid off tomorrow, these bills still demand payment. This half of your income keeps a roof over your head and food on the table.

Here is what belongs in your 50% bucket:

Allocating your “Wants” (30%)

Guilt-free Spending

You work hard. Budgeting fails the moment it feels like a punishment. If you eliminate all joy from your life, you will inevitably binge-spend and ruin your financial goals. This 30% bucket is your permission slip to enjoy your sweldo guilt-free.

This is your money to burn. Enjoy it.

Securing your Savings (20%)

Debts and Future-building

This is how you escape the rat race. You must pay yourself first. The moment your salary hits your account, transfer this 20% out immediately. Do not wait to see “what is left” at the end of the month. Nothing is ever left.

How to Budget Salary in the Philippines Using the 50/30/20 Rule

Step 1: Compute your real take-home pay

Before allocating percentages, calculate your net income (after deductions).

Common Philippine payroll deductions include:

- SSS contributions – Social Security System

- PhilHealth contributions – PhilHealth

- Pag-IBIG contributions – Pag-IBIG Fund

- Withholding tax (BIR)

Always budget using net pay, not gross salary.

Step 2: Allocate 50% to Needs

Needs are non-negotiable expenses required for survival and work.

Step 3: Allocate 30% to Wants

Wants improve quality of life but are optional:

This is your guilt-free spending zone.

Step 4: Allocate 20% to Savings & Investments

This is where wealth building starts.

Budgeting a ₱30,000 Monthly Salary in the Philippines (Example)

Let’s look at the actual math. Theory is useless without application. Say you earn ₱30,000 a month. Remember, this is your net take-home pay after the BIR, PhilHealth, Pag-IBIG, and SSS have taken their share.

Here is exactly how that money gets divided under the 50/30/20 framework.

|

Category |

Percentage |

Allocation |

Real-Life Expenses |

|---|---|---|---|

|

Needs |

50% |

₱15,000 |

|

|

Wants |

30% |

₱9,000 |

|

|

Savings/Debt |

20% |

₱6,000 |

|

Look at how clean that is. You still get ₱9,000 just to enjoy your life. You do not have to feel guilty about ordering that iced coffee or buying a new shirt. The math already gave you permission. At the exact same time, you are consistently dropping ₱6,000 into your future. Every single month.

4 Budgeting Tips Pinoy Professionals Actually Use

Here are practical budgeting tips Pinoy earners follow:

1. Automate your savings first

Set up an auto transfer to your savings account immediately after payday. 20% of your income should go directly without you ever touching it.

2. Use separate accounts

3. Track weekly, not monthly

Monthly tracking is too late. Weekly keeps you accountable.

4. Avoid lifestyle inflation

When salary increases, raise your savings rate, not just your spending.

5. Build Emergency Fund Before Investing

According to global financial planning standards (CFP Board), emergency funds should cover 3 to 6 months of expenses before aggressive investing.

Budgeting for Irregular Income (Freelancers & Commission-Based Workers)

If you’re a freelancer:

Irregular earners should prioritize liquidity.

3 Common Pinoy Budgeting Traps

And how to avoid them

The math works. The spreadsheet is flawless. But human behavior ruins the spreadsheet. Here are the three biggest cultural traps Filipinos fall into, and exactly how you beat them.

The “Dasurv Ko ‘To” Mentality

You survived a brutal work week. Your client yelled at you. The MRT broke down twice. Payday finally arrives, and you immediately blow half your sweldo on a massive weekend trip or an expensive gadget because you feel you “deserve it.” This is revenge spending. It destroys your 30% wants bucket instantly.

The Fix: Automate your savings the minute you get paid. Open a separate digital bank account specifically for your 20% bucket. The moment your salary hits your main account, transfer that 20% out immediately. You cannot revenge-spend money you do not see.

The “Black Tax” (Family Obligations)

This is the hardest conversation to have. In the Philippines, the breadwinner often supports parents, siblings, and sometimes extended relatives. You want to help. But draining your own emergency fund to pay your cousin’s tuition keeps everyone trapped in the cycle of poverty.

The Fix: Treat your family padala as a fixed line item. Decide right now: does this money come out of your 50% Needs or your 30% Wants? Cap the amount. You cannot pour from an empty cup. You have to secure your own 20% savings first before you can effectively help anyone else.

Confusing Needs and Wants

We lie to ourselves. You convince yourself that the latest iPhone is a “need” for your side hustle. You justify taking a Grab car every single day because you “need” the extra sleep. Suddenly, your 50% Needs bucket swells to 85%, and you have zero cash left for savings.

The Fix: Be ruthlessly honest with your money. A roof over your head is a need. A condo with a pool is a want. Rice, vegetables, and chicken are needs. A daily ₱200 coffee shop run is a want. Downgrade your lifestyle until your true survival needs actually fit inside that 50% boundary.

What if My Salary is Too Low for the 50/30/20 Rule?

Let’s be brutally honest. Inflation is ruthless. The math does not always cooperate with reality.

If you are earning minimum wage in Metro Manila, 50% of your take-home pay will simply not cover your rent, your Meralco bill, and your daily MRT commute.

You might calculate your basic survival expenses and realize they eat up 75% or 80% of your income.

Do not panic. And absolutely do not starve yourself just to hit a spreadsheet target.

If your income is currently too low for the 50/30/20 split, adjust the ratio to fit your reality.

The specific percentages matter less than the habit. You are training your brain to categorize money the second it hits your bank account. Build the discipline now while your salary is small.

Simultaneously, make it your mission to outgrow this phase. You cannot budget your way out of poverty if the income itself is fundamentally broken.

Upskill. Take freelance clients. Build a side hustle.

Once your income increases, do not inflate your lifestyle. Keep your needs fixed, and pour that new money directly into your 20% savings bucket.

Frequently Asked Questions

Is the 50/30/20 rule realistic in the Philippines?

Yes, but percentages may need adjustment depending on income level and location. You can use 60-20-20 or 70-20-10 depending on your financial situation.

How do I budget if I earn below ₱20,000?

Start with 70/20/10 or 80/10/10. Focus on building stability first.

Should I save or pay debt first?

High-interest debt (like credit cards) should be prioritized before investing.

Is 20% savings enough?

It’s a strong starting point. Increasing to 30–40% accelerates financial independence.

Final Thoughts

Start your “Ipon” Journey

The 50/30/20 rule isn’t magic.

It won’t double your salary. It won’t instantly make you rich.

But it will give your money direction.

And that’s what most people are missing: structure.

When you assign every peso a role, you stop wondering where your money went.

And over time, those small, consistent decisions compound.

You do not need a 6-figure salary to build wealth. You just need boundaries.

Do not wait for the “perfect” time to start. Do not wait for your next promotion or your 13th-month pay. Start with your very next paycheck.

Once you automate that single decision, the rest of your financial life will slowly fall into place.

Ready to take the next step? Head back to our Ultimate Guide to Personal Finance in the Philippines to map out the rest of your wealth-building strategy.