Best Index Funds in the Philippines (2026): Top PSEi Index Funds Compared

Written by

Paul Daveril Dabuco

Founder, Juan Investor • Digital marketing expert and investor

Paul bought his first stock in 2013 and has spent the decade since compounding and making the expensive mistakes he now writes about so you can skip them. Read my profile.

Paul Daveril Dabuco is the founder and author of Juan Investor. He started investing in stocks in 2013 and currently holds a portfolio of stocks, crypto and index fund investments. When he’s not blogging he’s either tinkering on Facebook ads or exploring white sand beaches across the globe.

FOLLOW me

Disclaimer: This post is not a financial or investing advice, it’s for educational purposes only. It may contain affiliate links, meaning I get a commission if you decide to make a purchase, at no extra cost to you. Read our disclosure

If you want to grow your wealth without picking individual stocks, investing in an index fund is one of the simplest strategies available. Instead of trying to beat the market, index funds aim to match the performance of a stock market index, making them a popular choice for long-term, passive investors.

This guide compares the best index funds in the Philippines to help you find the right option for your investing goals. We’ll look at exchange-traded funds (ETFs), unit investment trust funds (UITFs), and mutual funds, explain their key differences, and show you how to choose the one that best fits your investing style.

Whether you’re investing your first ₱1,000 or building a long-term retirement portfolio, this guide will help you make a more informed decision.

For most Filipino investors, the best index fund depends on how you plan to invest rather than a single “best” fund.

The most important factor isn’t finding the fund with the highest recent return. It’s choosing a low-cost index fund that you’ll consistently invest in for many years.

Best index funds in the Philippines compared

|

Index fund |

Fund type |

Benchmark |

Typical minimum investment* |

Best for |

|---|---|---|---|---|

|

First Metro Philippine Equity Exchange Traded Fund (FMETF) |

ETF |

PSEi |

Price of 1 share |

DIY investors using a stock brokerage |

|

BPI Invest Philippine Equity Index Fund |

UITF |

PSEi |

Low |

Beginners and existing BPI clients |

|

BDO Equity Index Fund |

UITF |

PSEi |

Low |

Existing BDO clients |

|

Metro Philippine Equity Index Fund |

UITF |

PSEi |

Moderate |

Metrobank customers |

|

Security Bank Equity Index Fund |

UITF |

PSEi |

Moderate |

Security Bank clients |

|

ATRAM Philippine Equity Smart Index Fund |

Mutual Fund |

Rules-based Philippine equity index |

Varies |

Investors seeking an alternative indexing approach |

*Minimum investment requirements, management fees, and fund availability may change over time. Always verify the latest details with the fund provider before investing.

Juan Investor Insight: Many beginners spend too much time trying to identify the “perfect” index fund. In reality, the long-term difference between two well-managed, low-cost PSEi index funds is often much smaller than the difference created by investing consistently every month for 10 to 20 years. Choosing a suitable fund and staying invested usually matters more than chasing small differences in short-term performance.

Our Picks: Best Philippine index funds

Not all index funds are created equal. While most Philippine index funds aim to track the Philippine Stock Exchange Index (PSEi), they differ in cost, accessibility, convenience, and how closely they follow the index over time.

Rather than declaring a single winner, we’ve selected the best index funds based on different investor needs. This approach makes it easier to choose a fund that fits your investing style instead of simply following the most popular option.

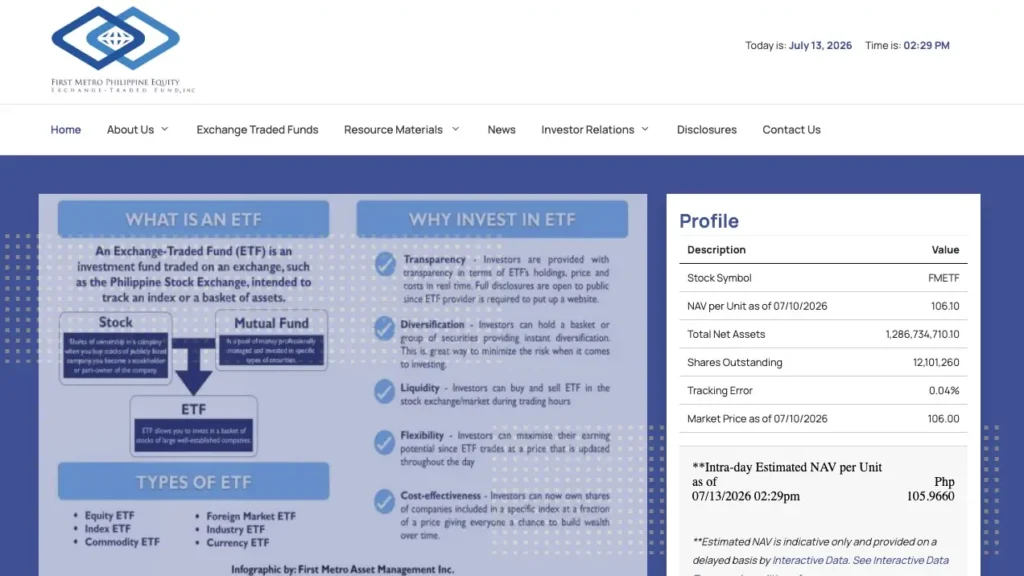

First Metro Philippine Equity Exchange Traded Fund (FMETF)

FMETF is the Philippines’ first and currently only exchange-traded fund (ETF). Unlike UITFs and mutual funds, you buy and sell FMETF shares through the Philippine Stock Exchange using a stock brokerage account.

Because it is traded like a stock, you can purchase shares anytime during market hours instead of waiting for the fund’s end-of-day net asset value (NAV).

For many long-term investors, FMETF is often the closest Philippine equivalent to buying an S&P 500 ETF in the United States.

Why we like it

Things to consider

Choose FMETF if…

BPI Invest Philippine Equity Index Fund

If convenience is your top priority, BPI’s Philippine Equity Index Fund is one of the easiest ways to begin passive investing.

Instead of opening a brokerage account, you invest directly through BPI’s trust platform. Existing BPI clients can usually monitor and manage their investments alongside their banking accounts, making the process more straightforward for first-time investors.

Why we like it

Things to consider

Choose this fund if…

BDO Equity Index Fund

The BDO Equity Index Fund offers another straightforward path to passive investing through a major Philippine bank.

Its primary objective is to mirror the performance of the PSEi, giving investors diversified exposure to many of the country’s largest publicly listed companies.

If you already use BDO’s online banking ecosystem, investing can feel familiar and convenient.

Why we like it

Things to consider

Choose this fund if…

Metro Philippine Equity Index Fund

Metrobank’s index fund provides another passive option for investors who want exposure to the Philippine stock market without selecting individual companies.

Like other index UITFs, its goal is to closely follow the performance of the PSEi while offering the convenience of investing through an established banking institution.

Why we like it

Things to consider

Choose this fund if…

Security Bank Equity Index Fund

Security Bank also offers a passive equity index fund designed to follow the PSEi.

Although it receives less attention than larger bank offerings, it remains a reasonable option for investors who value convenience and already have an investment relationship with Security Bank.

Why we like it

Things to consider

Choose this fund if…

ATRAM Philippine Equity Smart Index Fund

Unlike funds that simply replicate the PSEi, ATRAM’s Smart Index Fund follows a rules-based methodology that selects Philippine equities according to predefined investment factors rather than purely market capitalization.

This approach seeks to improve diversification while maintaining a disciplined, passive investment process.

Why we like it

Things to consider

Choose this fund if…

Juan Investor Insight: The “best” index fund is rarely the one with the highest return over the past year. A better way to choose is to compare fees, tracking consistency, accessibility, and how likely you are to keep investing consistently. An investor who faithfully contributes to a good index fund every month for 20 years will often outperform someone who constantly switches funds in search of last year’s best performer.

How we evaluated these index funds

Many “best index funds” articles simply rank funds based on historical returns. We don’t think that’s the best approach.

An index fund’s purpose isn’t to beat the market. It’s to track the market consistently while keeping costs low. A fund that tops the performance charts one year may not remain the leader over the next decade.

Instead, we evaluated each fund using what we call the Juan Investor Index Fund Scorecard. This framework focuses on the factors that matter most to long-term investors.

|

Evaluation factor |

Why it matters |

|---|---|

|

Tracking accuracy |

A good index fund should closely follow the performance of its benchmark, with minimal tracking error. |

|

Fees and expenses |

Lower management fees mean more of your investment stays invested and compounds over time. |

|

Accessibility |

We considered how easy it is to open an account, meet the minimum investment, and start investing. |

|

Convenience |

We looked at the overall investing experience, including online access, regular investment options, and ease of managing the fund. |

|

Long-term suitability |

We favored funds designed for disciplined, buy-and-hold investors rather than short-term traders. |

Juan Investor Insight: Think of choosing an index fund like choosing a vehicle for a long road trip. Fuel efficiency, reliability, and ease of maintenance matter far more than which car accelerates the fastest. Likewise, low fees, consistent tracking, and a platform you’ll actually use are usually more important than chasing the fund with last year’s highest return.

How to choose the right index fund

There’s no single “best” index fund for everyone. The right choice depends on your investing habits, preferred platform, and long-term goals.

Instead of asking, “Which index fund has the highest return?”, ask “Which index fund am I most likely to keep investing in for the next 10 to 20 years?”

That’s usually the better question.

Use the Juan Investor Index Fund Decision Framework.

Ask yourself these five questions before investing.

Do you want to invest through a bank or a stock brokerage?

This is often the biggest deciding factor.

If you prefer managing your investments alongside your savings account, a UITF or mutual fund offered by your bank may be the most convenient option.

If you’re comfortable using a stock brokerage and want more control over buying and selling, FMETF may be a better fit.

How important are low fees?

Index investing is built on the idea that keeping costs low helps maximize long-term returns.

If two funds aim to track the same index, the one with lower ongoing expenses generally has a slight advantage over time, assuming both track the benchmark effectively.

That doesn’t mean you should choose the cheapest fund automatically. Consider whether the cost savings outweigh the added convenience offered by your preferred bank or investment platform.

Will you invest regularly?

Successful index investing depends more on consistency than timing.

If your bank allows you to invest automatically every payday, that convenience can make it easier to stick to your plan. For many investors, a simple monthly investment habit is more valuable than trying to buy only when the market falls.

How closely does the fund track its benchmark?

Two index funds following the PSEi won’t always deliver identical returns.

Small differences are expected because of management fees, transaction costs, and portfolio management. However, a fund that consistently lags far behind its benchmark may deserve closer examination.

When comparing similar funds, look beyond performance over the last year. Review how consistently the fund has tracked its benchmark across multiple years.

Will this fund fit your long-term strategy?

An index fund should be part of a broader financial plan.

Before investing, ask yourself:

If your answer is “yes” to most of these questions, an index fund can be an excellent foundation for long-term wealth building.

A simple decision guide

|

If your priority is… |

Consider… |

|---|---|

|

Lowest ongoing costs and flexibility |

FMETF |

|

Easy investing through your bank |

A UITF from your preferred bank |

|

Automatic, long-term monthly investing |

A bank UITF with regular investment options |

|

Buying and selling during market hours |

FMETF |

|

Keeping all your finances in one institution |

Your existing bank’s index fund |

Juan Investor Insight: Many investors spend weeks comparing two index funds whose long-term returns may differ only slightly. A more productive use of that time is building the habit of investing every month. Consistency usually has a much greater impact on your portfolio than choosing between two similar PSEi index funds.

Mutual fund vs UITF vs ETF

One reason choosing an index fund in the Philippines can feel confusing is that index investing is available through three different investment vehicles: mutual funds, UITFs, and ETFs.

Although they can all provide diversified exposure to the stock market, they work differently.

|

Feature |

Mutual fund |

|---|---|

|

Managed by |

Investment company |

|

Bought through |

Investment company or distributor |

|

Trading |

End-of-day NAV |

|

Pricing |

Once daily |

|

Liquidity |

Redeem through fund company |

|

Best for |

Long-term investors |

Mutual funds

A mutual fund pools money from many investors and invests it according to a specific objective.

An index mutual fund follows a passive strategy by tracking a market index instead of relying on a fund manager to pick winning stocks.

Mutual funds are generally easy to access and are designed for long-term investing rather than frequent trading.

UITFs

A Unit Investment Trust Fund (UITF) is similar to a mutual fund, but it is offered and managed by a bank’s trust department.

For many Filipinos, UITFs provide the simplest entry into investing because they can often be opened through an existing banking relationship.

ETFs

An Exchange Traded Fund (ETF) combines features of both mutual funds and individual stocks.

Instead of subscribing directly through a bank or investment company, you buy ETF shares on the Philippine Stock Exchange using a brokerage account.

Because ETFs trade throughout the day, you can buy or sell whenever the market is open. Their prices also change continuously based on supply and demand.

Which one should you choose?

Each investment vehicle serves a different type of investor.

- Choose an ETF if you’re comfortable using a stock brokerage and want the flexibility to trade during market hours.

- Choose a UITF if convenience and simplicity are your priorities, especially if you already have a relationship with a bank.

- Choose an index mutual fund if it offers competitive fees, fits your preferred investment platform, and aligns with your long-term strategy.

The good news is that there isn’t a wrong choice among these options if you’re investing consistently in a well-managed, low-cost index fund.

The investment vehicle matters, but your saving habit, investment discipline, and long-term mindset will have a much bigger influence on your financial results.

Common mistakes when choosing an index fund

Index investing is one of the simplest ways to build wealth, but it’s still possible to make costly mistakes. Fortunately, most of them are easy to avoid once you know what to look for.

Chasing the highest recent returns

One of the biggest mistakes beginners make is choosing the fund that performed best over the past year.

Past performance can provide useful context, but it doesn’t guarantee future results. Markets move in cycles, and last year’s top-performing fund may not remain the leader in the years ahead.

Instead of focusing on short-term returns, compare factors such as fees, tracking consistency, and whether the fund fits your long-term investment strategy.

Ignoring management fees

A difference of half a percentage point in annual fees may not seem significant today, but it can have a meaningful impact after years of compounding.

Lower costs allow more of your investment to remain in the market, which is one of the core principles of passive investing.

When comparing similar index funds, always review the fund’s fees alongside its investment objective and benchmark.

Investing without an emergency fund

An index fund is designed for long-term investing.

If you might need the money within the next few months, you could be forced to sell your investment during a market downturn.

Building an emergency fund first gives your investments time to recover from temporary declines and reduces the likelihood of selling at the worst possible moment.

Expecting quick profits

The Philippine stock market can experience periods of strong growth, but it can also go through years of weak or negative returns.

Index funds are not designed to generate quick profits.

They’re designed to help investors participate in the long-term growth of the market.

Patience is one of the biggest advantages an individual investor has.

Trying to time the market

Many investors wait for the “perfect” time to invest.

Unfortunately, nobody can consistently predict when the market will reach its highest or lowest point.

A more practical approach is to invest regularly through peso-cost averaging. This strategy removes much of the emotion from investing and helps build discipline over time.

Switching funds too often

Changing index funds every time another fund outperforms can increase costs and reduce the benefits of a long-term strategy.

Remember that all PSEi index funds are trying to achieve a similar objective. Once you’ve chosen a suitable, low-cost fund, your attention is usually better spent increasing your investment contributions instead of constantly changing funds.

Juan Investor checklist: Before investing, ask yourself:

If you can answer “yes” to these questions, you’re already avoiding many of the mistakes that derail new investors.

Frequently asked questions

Which is the best index fund in the Philippines?

FMETF is often preferred by DIY investors who use a stock brokerage, while bank UITFs from providers such as BPI and BDO are excellent options for investors who value convenience and automatic investing.

Is FMETF better than a UITF?

Neither is universally better. FMETF generally offers greater flexibility because it trades on the Philippine Stock Exchange and may have lower ongoing costs. A UITF, however, may be more convenient if you already invest through your bank and prefer a simpler investment experience.

What is the minimum investment for an index fund?

For FMETF, you’ll need enough funds to purchase at least one share plus applicable trading costs. UITFs and mutual funds have their own minimum initial and subsequent investment requirements, so it’s best to check with the fund provider before investing.

Are index funds safe?

Index funds are generally considered less risky than investing in individual stocks because they provide instant diversification across multiple companies. However, they are still equity investments. Their value can rise and fall with the stock market, and there is no guarantee of positive returns over short periods.

How long should I hold an index fund?

Index funds are best suited for long-term goals. Many financial planners recommend investing with a time horizon of at least 5 years, while investors saving for retirement often remain invested for decades.

Can beginners invest in index funds?

Yes. In fact, index funds are often recommended as one of the best starting points for beginner investors because they offer diversification, require little ongoing management, and encourage a disciplined, long-term investing approach.

Conclusion

Index funds are one of the simplest and most effective ways to start investing in the stock market.

Rather than trying to predict which company will become the next big winner, an index fund lets you own a diversified portfolio of many of the country’s largest publicly listed companies through a single investment.

The key is not to find the “perfect” fund.

It’s to choose a well-managed, low-cost index fund that fits your investing style, then commit to investing consistently over the long term.

Whether you decide on FMETF, a bank UITF, or an index mutual fund, your success will depend far more on your discipline than on small differences between similar funds.

If you’re just beginning your investing journey, start by building a strong financial foundation, invest only money you won’t need in the near future, and focus on consistency instead of short-term market movements.

Related articles:

- Best mutual funds in the Philippines

- Best investments in the Philippines

- How to start investing in the Philippines

Subscribe to Juan Investor

Be the first to know when a new article (or a giveaway) is out. No spam.